Accounting For Share Capital

53 previous year questions.

High-Yield Trend

Chapter Questions 53 MCQs

Reason (R): Securities Premium can be applied only for the purposes mentioned in the Companies Act, 2013.

Choose the correct option from the following:

Answer the following questions:

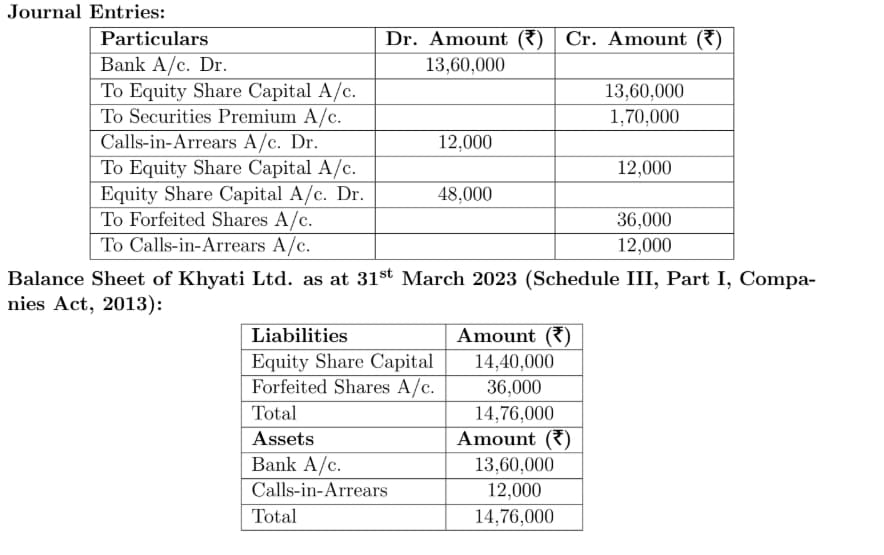

(i) The amount of ‘Calls in Arrears’ disclosed in ‘Notes to Accounts’ will be :

(A) ₹ 1,40,000 (B) ₹ 36,000 (C) ₹ 4,000 (D) Nil

(ii) The number of shares of LK Ltd. after forfeiture will be :

(A) 1,46,000 (B) 1,36,000 (C) 1,41,000 (D) 1,40,000

(iii) In the ‘Notes to Accounts’, the amount disclosed under ‘Share Forfeiture Account’ will be :

(A) ₹ 4,000 (B) ₹ 36,000 (C) ₹ 40,000 (D) Nil

(iv) In the ‘Notes to Accounts’, the amount disclosed under ‘Issued Capital’ will be :

(A) ₹ 14,00,000 (B) ₹ 14,50,000 (C) ₹ 15,00,000 (D) ₹ 13,60,000

(v) Balance in ‘Share Forfeiture Account’ will be shown in ‘Notes to Accounts’ in the balance sheet of LK Ltd. under :

(A) Subscribed capital (B) Will not be shown in ‘Notes to Accounts’

(C) Issued capital (D) Authorised capital

(vi) The amount of ‘Share Capital’ disclosed in the balance sheet of LK Ltd. will be :

(A) ₹ 13,56,000 (B) ₹ 13,64,000 (C) ₹ 13,96,000 (D) ₹ 14,00,000

On Application and Allotment – ₹ 40 per share (including ₹ 10 premium)

On First call – ₹ 45 per share (including ₹ 5 premium)

On Second and final call – Balance

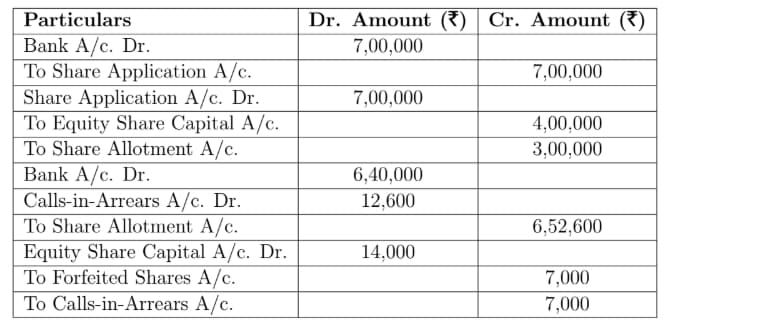

Applications for 39,000 shares were received. Allotment was made in full to all the applicants. Dinu, to whom 100 shares were allotted, failed to pay the first call money. His shares were immediately forfeited. The forfeited shares were re-issued thereafter at ₹ 70 per share fully paid up. The second and final call was not yet made. Pass necessary journal entries for the above transactions in the books of Radhika Ltd.

On First and Final call – ₹ 10 per share (including premium ₹ 3 per share)

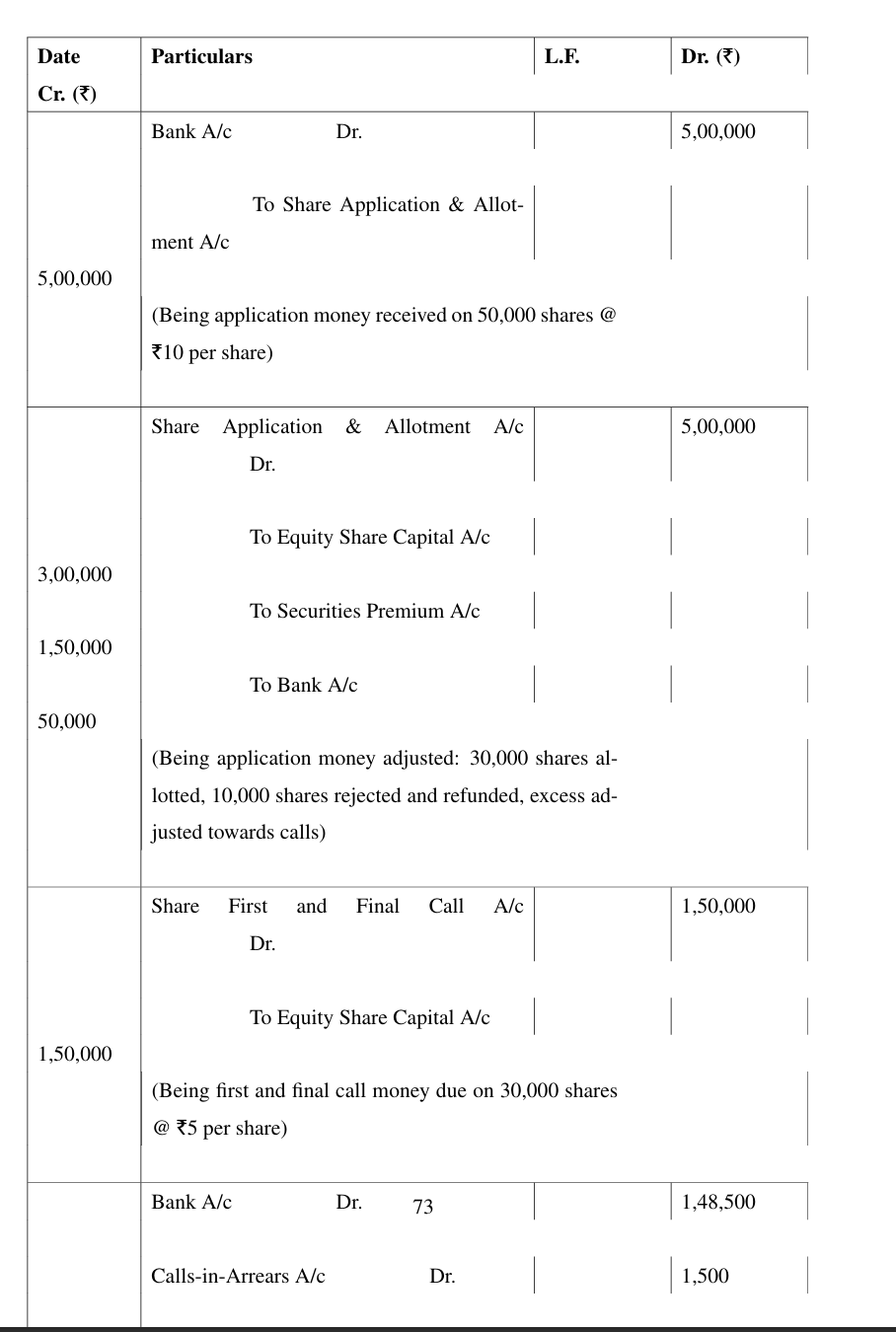

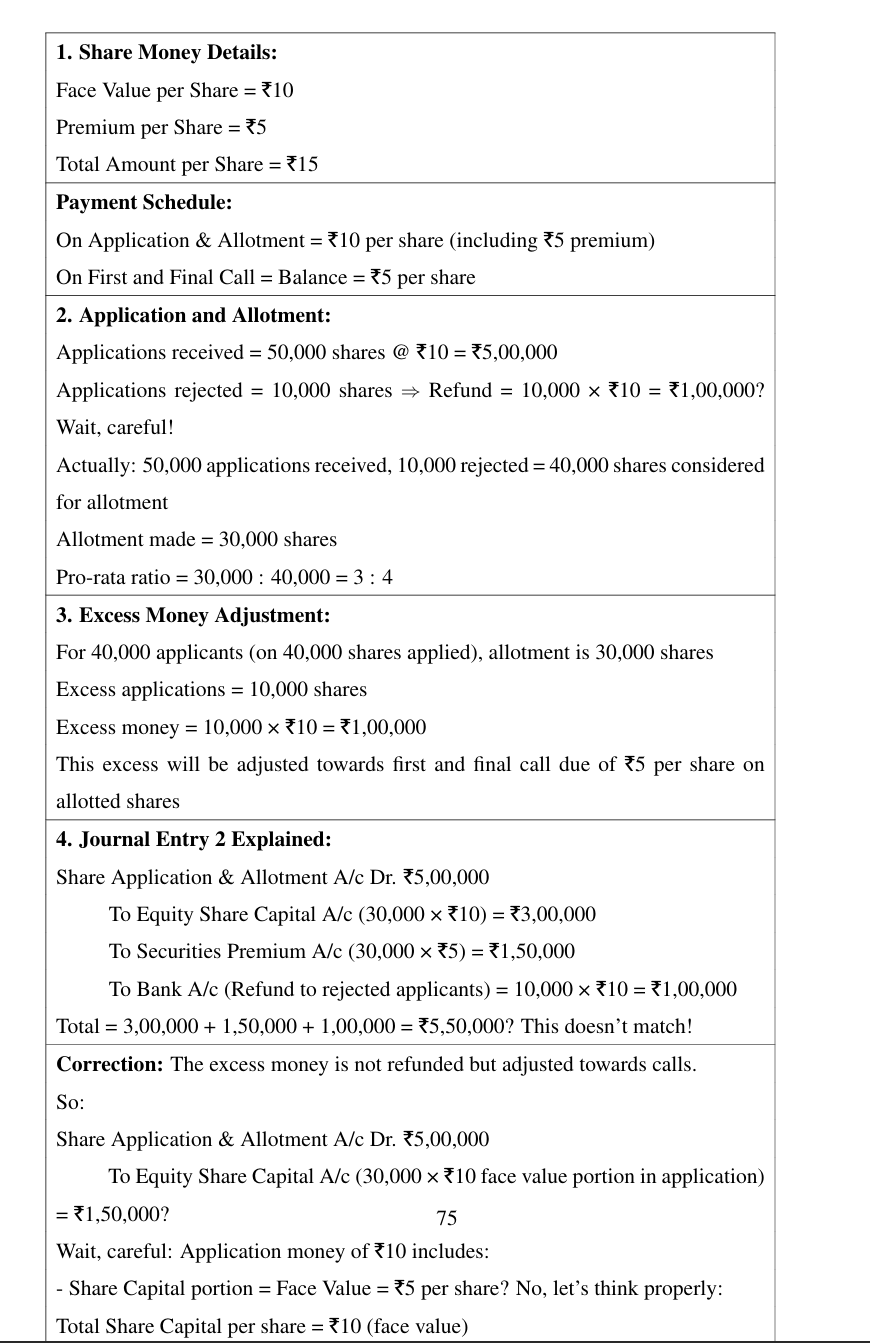

Applications were received for 3,00,000 equity shares and allotment was made to the applicants as follows: (i) Applicants for 2,00,000 shares were allotted 1,50,000 shares.

(ii) Applicants for 1,00,000 shares were allotted 50,000 shares.

Excess money received on application and allotment was adjusted towards sums due on first and final call. Deepali, who had applied for 2,000 shares, failed to pay the first and final call money. Her shares were subsequently forfeited. Deepali belonged to Category (i).

Pass necessary journal entries for the above transactions in the Books of Centurian Ltd.

Open Calls-in-Arrears and Calls-in-Advance account, wherever necessary.

(i) Macil Ltd. forfeited 3,000 shares of ₹ 100 each issued at 20% premium for non-payment of allotment ₹ 30/share and 1st call ₹ 40/share (incl. premium ₹ 10). 2nd and final call of ₹ 30 not yet called. Out of these, 2,000 were reissued at ₹ 80 each fully paid up for ₹ 90/share.

(ii) Avian Ltd. forfeited 10,000 shares of ₹ 10 each. First call of ₹ 4 not received, second and final call of ₹ 1 not yet called. 4,000 shares reissued to Ajay at ₹ 9 fully paid.

% [Balance Sheet Extract & Notes shown in Question] Notes to accounts' as at 31st March, 2023 \& 2024 show changes in Share Capital.

Analysis from Notes:

As at 31-3-2023: Issued \& Subscribed Capital: 5,00,000 equity shares of Rs 10 each, fully paid up = Rs 50,00,000.

As at 31-3-2024: Issued Capital: 6,00,000 equity shares of Rs 10 each. Subscribed: 5,80,000 shares fully paid up (Rs 58,00,000) + 20,000 shares fully called up (Rs 2,00,000) less Calls in Arrears (Rs 40,000 on 20,000 shares @ Rs 2) = Rs 1,60,000. Total Subscribed = Rs 59,60,000.

Answer the following questions :

(i) The total face value of equity shares issued during the year 2023-2024 was:

On application and allotment – ₹ 7 (incl. ₹ 1 premium)

On first and final call – Balance.

Applications received for 2,40,000 shares. 30,000 rejected. Manvi allotted 4,000 shares failed to pay first and final call. Her shares were forfeited. These were reissued at ₹ 4 per share fully paid-up.

Pass journal entries in the books of Altima Ltd.

On Application – ₹ 20 per share

On Allotment – ₹ 25 per share

On First and final call – Balance

Applications for 90,000 shares were received. Applications for 10,000 shares were rejected and application money refunded. Shares were allotted on pro-rata basis to the remaining applicants. Excess money received with applications was adjusted towards sums due on allotment. Rahul, to whom 600 shares were allotted, failed to pay the allotment money and his shares were forfeited immediately. Afterwards, the first and final call was made. Mona, to whom 1,000 shares were allotted, failed to pay the first and final call. Her shares were also forfeited. Pass necessary journal entries in the books of Sona Ltd. for the above transactions.

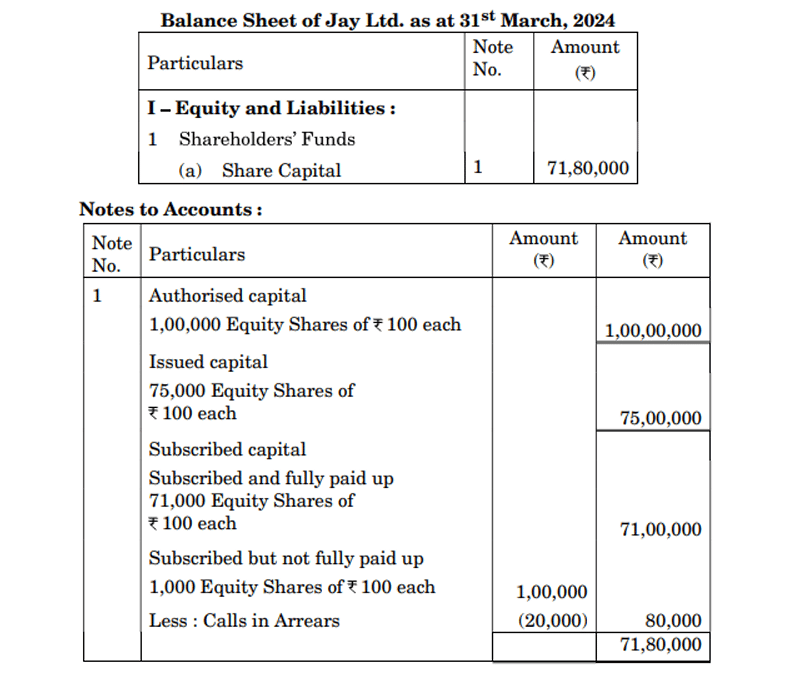

Following is the extract of the Balance Sheet of Sankalp Ltd. as per Schedule III, Part I of the Companies Act, 2013 as at 31st March, 2024 along with the notes to accounts: Balance Sheet of Sankalp Ltd. as at 31st March, 2024 (An extract)}

| Particulars | 31.03.2024 (₹) | 31.03.2023 (₹) |

|---|---|---|

| I – Equity and Liabilities | ||

| 1. Shareholders’ Funds | ||

| (a) Share Capital | 29,80,000 | 25,00,000 |

Notes to Accounts as at 31 st March, 2023

| Particulars | 31.03.2023 (₹) |

|---|---|

| Authorised Capital 4,50,000 Equity Shares of ₹10 each | 45,00,000 |

| Issued Capital 2,50,000 Equity Shares of ₹10 each | 25,00,000 |

| Subscribed Capital Subscribed and fully paid-up 2,50,000 Equity Shares of ₹10 each | 25,00,000 |

| Subscribed but not fully paid-up | NIL |

| Total | 25,00,000 |

Notes to Accounts as at 31st March, 2024

| Particulars | 31.03.2024 (₹) |

|---|---|

| Authorised Capital 4,50,000 Equity Shares of ₹10 each | 45,00,000 |

| Issued Capital 3,00,000 Equity Shares of ₹10 each | 30,00,000 |

| Subscribed Capital Subscribed and fully paid-up 2,90,000 Equity Shares of ₹10 each | 29,00,000 |

| Subscribed but not fully paid-up 10,000 Equity Shares of ₹10 each fully called-up | 1,00,000 |

| Less: Calls-in-Arrears 10,000 Equity Shares @ ₹2 per share | 20,000 |

| Total | 29,80,000 |

Answer the following questions:

PR Ltd. forfeited 10,000 equity shares of ₹10 each, issued at a premium of ₹4 per share, for non-payment of the first call of ₹3 per share. The second and final call of ₹2 per share had not yet been made.

These forfeited shares were later reissued at a discount of ₹1 per share, fully paid-up.

Pass necessary journal entries for the forfeiture and reissue of shares in the books of PR Ltd. Also prepare the Share Forfeiture Account.

Devi and Anupam were partners in a firm. Their fixed capitals were ₹9,00,000 and ₹6,00,000 respectively on 1st April, 2023. The partnership deed provided for the following:

(i) Interest on capital @ 12% p.a.

(ii) Interest on drawings @ 15% p.a.

On 1st May, 2023, Devi introduced additional capital of ₹1,00,000 and on 1st June, 2023, Anupam withdrew ₹2,00,000 from her capital.

Devi withdrew ₹4,000 per month for her personal use and Anupam withdrew ₹2,000 per month for her personal use.

The net divisible profit of the firm for the year ended 31st March, 2024 after allowing interest on capital and charging interest on drawings was ₹3,00,000.

Prepare Current Accounts of the partners.

Statement-I: Snow Limited earned a profit of Rs 2,00,000 after charging depreciation of Rs 50,000 on machinery. So, operating profit before working capital changes would be Rs 2,50,000.

Statement-II: Depreciation is added back to net profit as it does not result in any cash flow.

On First call – ₹ 40 per share

On Second and Final call – balance The issue was fully subscribed. All amounts were duly received except from Nawal, a shareholder holding 700 shares, who failed to pay the second and final call. His shares were forfeited. On the basis of the above information, answer the following questions: (i) The Registered capital of Diwan Ltd. is:

On first and final call – Balance Applications for 50,000 shares were received. Applications for 10,000 shares were rejected and their application money was refunded. Pro-rata allotment was made to the remaining applicants. Excess money received with application was adjusted towards sums due on first and final call. Sonu, an applicant of 4,000 shares, paid his entire share money with application. Vedika, to whom 300 shares were allotted, failed to pay the first and final call. After giving her the mandatory notice, her shares were forfeited. Pass necessary journal entries for the above transactions in the books of Ajanta Ltd.

About Accounting For Share Capital - CBSE-CLASS-XII

Accounting For Share Capital is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Accounting For Share Capital PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Accounting For Share Capital carry the most weight. Then, tackle the questions iteratively to solidify your understanding.