Cash Flow Statement

33 previous year questions.

High-Yield Trend

Chapter Questions 33 MCQs

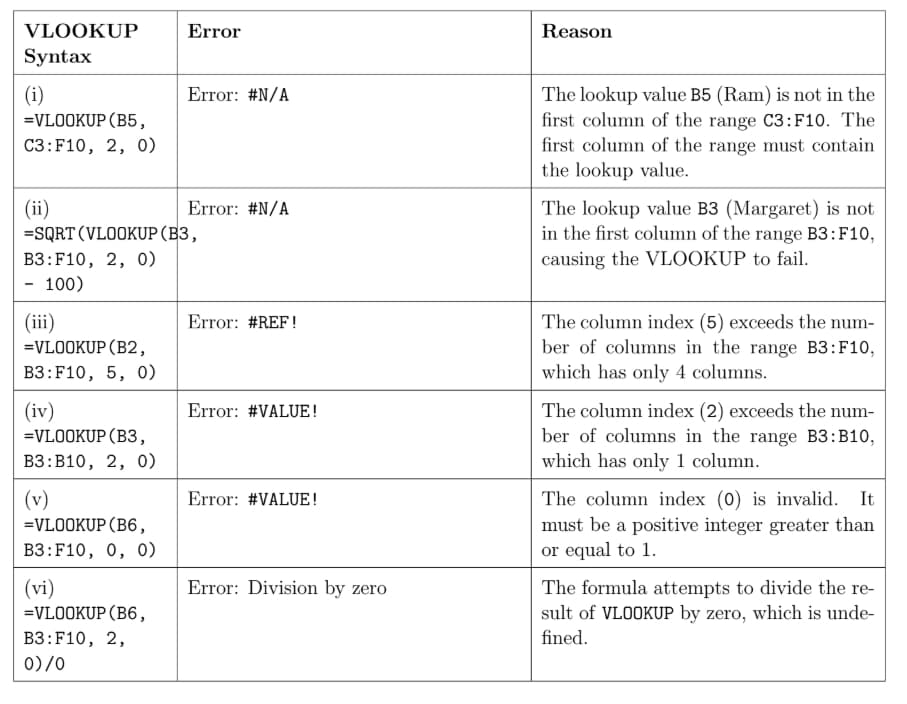

(i) = VLOOKUP(B5, C3:F10, 2, 0)

(ii) = SQRT(VLOOKUP(B3, B3:F10, 2, 0) - 100)

(iii) = VLOOKUP(B2, B3:F10, 5, 0)

(iv) = VLOOKUP(B3, B3:B10, 2, 0)

(v) = VLOOKUP(B6, B3:F10, 0, 0)

(vi) = VLOOKUP(B6, B3:F10, 2, 0)/0

Additional Information:

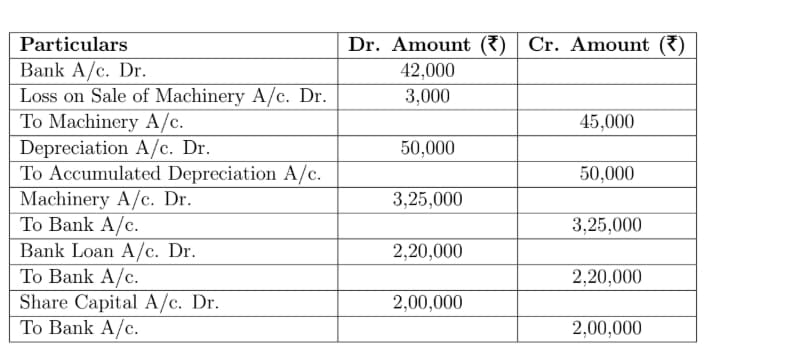

(i) rupee50,000 was charged as depreciation on Plant and Machinery. A machinery costing rupee60,000 (Book Value Rupees 45,000) was sold for Rupees 42,000.

(ii) Bank loan was repaid on 1st April, 2022.

Issue of 9% debentures of rupee 1,00,000 to the vendors of machinery

Redeemed 10% debentures by converting into equity shares

Both Financing & Operating activity

Statement II: To calculate operating profit, before working capital changes, interest on investment is subtracted from net profit because it is a non-operating income.

Choose the correct option:

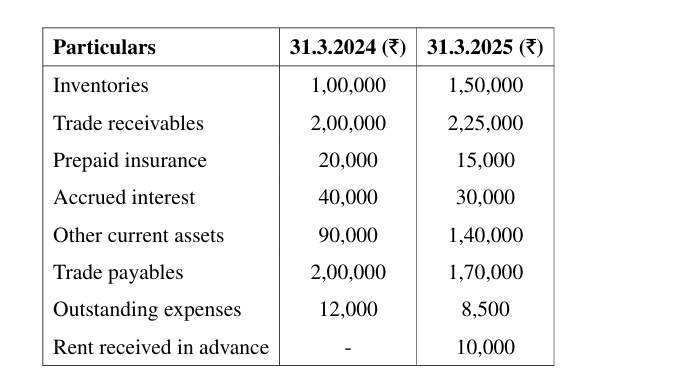

Comparative Financial Data as on 31st March, 2024 and 2023

| Particulars | 31.03.2024 (₹) | 31.03.2023 (₹) |

|---|---|---|

| Surplus (P&L) | 17,00,000 | 8,00,000 |

| Patents | -- | 50,000 |

| Sundry Debtors | 5,80,000 | 4,20,000 |

| Sundry Creditors | 1,40,000 | 60,000 |

| Cash and Cash Equivalents | 2,00,000 | 90,000 |

In case of non-financial enterprises, payment of interest and dividends are classified as financing activities, whereas receipt of interest and dividends are classified as investing activities.

Investing and financing transactions that require the use of cash or cash equivalents, should be excluded from cash flow statement.

Choose the correct alternative from the following:

Comparative Statement of Assets

| Particulars | 31.03.2024 (₹) | 31.03.2023 (₹) |

|---|---|---|

| 10% Long Term Investments | 2,50,000 | 4,50,000 |

| Plant and Machinery | 8,00,000 | 6,00,000 |

| Goodwill | 1,40,000 | 1,00,000 |

| Investment in shares of Pinnacle Ltd. | 14,00,000 | 5,00,000 |

| Patents | - | 1,50,000 |

| Particulars | 31-03-2024 (₹) | 31-03-2023 (₹) |

|---|---|---|

| Equity Share Capital | 12,00,000 | 8,00,000 |

| 11% Debentures | 3,00,000 | 4,00,000 |

| Securities Premium | 1,40,000 | 1,00,000 |

Interest paid on debentures amounted to ₹ 40,000.

| Particulars | 31-03-2024 (₹) | 31-03-2023 (₹) |

|---|---|---|

| Machinery (at cost) | 3,80,000 | 3,00,000 |

| Accumulated Depreciation | 62,000 | 45,000 |

A machine costing ₹ 50,000 on which accumulated depreciation was ₹ 20,000 was sold at a profit of 10%.

Statement– II : Cash payments to acquire fixed assets including intangibles and capitalised research and development results in cash outflow from investing activities.

Choose the correct option from the following :

Cash payments to suppliers for goods and services.

Dividend received from investments in other enterprises.

Cash receipts from royalties, fees, commissions and other revenues.

Cash repayments of amounts borrowed.

Cash payments to suppliers for goods and services.

Dividend received from investments in other enterprises.

Cash receipts from royalties, fees, commissions and other revenues.

Cash repayments of amounts borrowed.

- Sale of Land Rs 80,000

- Purchase of Investments Rs 50,000

- Interest received Rs 8,000

(a) Stock-in-trade

(b) Motor Vehicles

(c) Provision for tax

- Purchase of Machinery ₹1,60,000

- Sale of Machinery ₹40,000

- Interest Paid ₹10,000

- Dividend Paid ₹15,000

- Proceeds from Issue of Shares ₹2,00,000

- Proceeds from Long-Term Borrowings ₹50,000

From the following information extracted from the books of Kant Ltd., calculate ‘Cash Flows from Operating Activities’.

Statement II: Cash flow implies movement of cash in and out due to some non-cash items.

Choose the correct option from the following:

The excess of current assets over quick assets was represented by inventories which were Rs. 68,000.

Calculate:

[(i)] Current Assets

[(ii)] Quick Assets

[(iii)] Current Liabilities

\begin{tabular}{|l|r|r|} \hline Particulars & 31.3.2024 (Rs.) & 31.3.2023 (Rs.)

\hline Machinery (Cost) & 70,00,000 & 50,00,000

Accumulated Depreciation & 10,00,000 & 8,00,000

\hline \end{tabular} \vspace{0.25cm} Additional Information:

(i) During the year, a piece of machinery costing Rs. 1,40,000 on which accumulated depreciation was Rs. 90,000, was sold at a gain of Rs. 10,000.

(ii) Depreciation charged during the year amounted to Rs. 2,90,000.

Calculate: Cash Flows from Investing Activities

About Cash Flow Statement - CBSE-CLASS-XII

Cash Flow Statement is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Cash Flow Statement PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Cash Flow Statement carry the most weight. Then, tackle the questions iteratively to solidify your understanding.