Miscellaneous

270 previous year questions.

High-Yield Trend

Chapter Questions 270 MCQs

Sanju and Manju were partners in a firm sharing profits and losses in the ratio of 3:2. Their Balance Sheet on 31st March, 2023 was as follows:

Adjustments:

- Furniture was to be depreciated by ₹6,000.

- Investments were valued at ₹72,000.

- Plant and Machinery was taken over by Sanju and Manju in their profit-sharing ratio.

- Uday will bring in proportionate capital and ₹10,000 as his share of goodwill premium in cash.

Printkit Limited invited applications for issue of 80,000 equity shares of Rs 10 each. The amount was payable as follows:

- On Application: ₹ 3 per share

- On Allotment: ₹ 2 per share

- On First and Final Call: Balance

Applications for 1,50,000 shares were received. Applications for 10,000 shares were rejected, and pro-rata allotment was made to the remaining applicants as follows:

- Category A: Applicants for 80,000 shares were allotted 40,000 shares.

- Category B: Applicants for 60,000 shares were allotted 40,000 shares.

Excess money received on application was adjusted toward the amount due on allotment and first and final call. All the amounts due on allotment and first and final call were duly received

Madhu, Raj, Atul, and Prachi were partners in a firm sharing profit and losses in the ratio of 3:2:4:1. With effect from 1st April, 2023, they decided to share profits and losses equally. Their Balance Sheet showed a General Reserve of ₹1,00,000. The goodwill of the firm was valued at ₹20,00,000. Pass necessary journal entries for the above on account of change in the profit-sharing ratio. Show your working clearly.

On 1st January, 2023, Abhishek, a partner, advanced a loan of ₹ 3,00,000 to the firm. In the absence of a partnership agreement, the amount of interest on the loan for the year ending 31\textsuperscript{st} March, 2023 will be:

Reason (R): In a partnership firm, at the time of admission, the new partner acquires the right to share the assets and the profits of the partnership firm.

Choose the correct option from the following:

On 1st April, 2022, Mega Ltd. issued 30,000, 10% Debentures of ₹100 each at a discount of 10%. The total amount of interest due on debentures for the year ending 31st March, 2023 will be:}

Raju, Sohan, and Tina are partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. Tina is guaranteed a minimum amount of ₹40,000 as a share of profit every year. Any deficiency arising on that account shall be borne by Raju. If profit of the firm for the year ended 31st March, 2023 is ₹1,60,000, Raju will bear a deficiency of:

(A) credited by ₹ 7,000

(B) debited by ₹ 5,000

(C) credited by ₹ 5,000

(D) debited by ₹ 7,000

\hline (A) & Workmen Compensation Reserve A/c & 84,000 & 75,000

& To Workmen Compensation Claim A/c & &

& To Manu’s Capital A/c & 4,000 &

& To Sonu’s Capital A/c & 3,000 &

& To Rahul’s Capital A/c & 2,000 &

\hline (B) & Workmen Compensation Reserve A/c & 84,000 & 75,000

& To Workmen Compensation Claim A/c & &

& To Manu’s Capital A/c & 4,000 &

& To Sonu’s Capital A/c & 3,000 &

& To Rahul’s Capital A/c & 2,000 &

\hline (C) & Manu’s Capital A/c & 500 & 500

& To Rahul’s Capital A/c & &

\hline (D) & Workmen Compensation Reserve A/c & 84,000 & 75,000

& To Workmen Compensation Claim A/c & &

& To Manu’s Capital A/c & 4,000 &

& To Sonu’s Capital A/c & 3,000 &

& To Rahul’s Capital A/c & 2,000 &

\hline \end{tabular} \caption{Journal Entry for Workmen Compensation Reserve} \end{table}

}

is also known as Acid-Test Ratio.

Statement II: Issue of Debentures to the vendors for purchase of machinery will result in outflow of cash.

Choose the correct option from the following:

Pass the necessary journal entries for the following transactions on the dissolution of the partnership firm of Sharma and Verma after the various assets (other than cash and bank balance) and outside liabilities have been transferred to Realisation Account:

(i) Sharma paid creditors ₹ 34,000 in full settlement of their claim of ₹ 40,000.

(ii) Verma agreed to pay his wife’s loan of ₹ 8,000.

(iii) There was an old typewriter which had been written off completely from the books. It was estimated to realise ₹ 3,000. It was taken over by Verma at the estimated price less 20%.

(iv) Neelu, an old customer whose account for ₹ 1,500 was written off as bad debt in the previous year, paid 80% of the amount.

(v) Dissolution expenses amounting to ₹ 8,000 were paid by Sharma. (vi) Loss on realisation ₹ 40,000 was to be distributed between Sharma and Verma in their profit-sharing ratio of 3:2.

Pass necessary journal entries for issue of debentures for the following transactions:

(i) Suhavo Ltd. issued 10,000, 11% Debentures of ₹ 100 each at a discount of 10%, redeemable at a premium of 5%.

(ii) Mudit Ltd. issued 20,000, 9% Debentures of ₹ 100 each at a premium of 5%, redeemable at a premium of 10%.

(iii) Sudip Ltd. issued 30,000, 8% Debentures of ₹ 100 each at par, redeemable at a premium of 5%.

Using the worksheet, find out the error and its reason for the given 'VLOOKUP' syntax:

(i) =VLOOKUP(B1, B4 : D6, 2, 0)

(ii) =SQRT(VLOOKUP(C2, C2 : D8, 2, 0) – 100)

(iii) =VLOOKUP(B5, B6 : D8, 1, 0)

(iv) =VLOOKUP(B3, B2 : D8, 5, 0)

(v) =VLOOKUP(B5, B3 : D8, 0, 0)

(vi) =VLOOKUP(B2, B2 : D7, 2, 0)/0

From the following information, calculate the 'Proprietary Ratio':

Statement II: 'Cash withdrawn from bank' will result in inflow of cash.

In the context of the above two statements, choose the correct option:

On application – ₹ 5 per share On allotment – ₹ 1 per share On first and final call – Balance

(i) Neon Ltd. forfeited 2,000 shares of ₹ 10 each issued at a premium of ₹ 2 per share for non-payment of allotment money of ₹ 5 per share (including premium). The first and final call of ₹ 2 per share was not yet made. Out of these, 1,500 shares were reissued at ₹ 7 per share, ₹ 8 paid up.

(a) Pass journal entries for issue of debentures and for writing off 'Loss on Issue of Debentures' utilizing Securities Premium Account at the end of the first year itself.

Reason (R): When the shares are forfeited, all entries relating to the shares forfeited, except those relating to securities premium, already recorded in accounting records must be reversed.

Choose the correct option from the following:

Reason (R): In the ‘Fixed Capital Method’, all items like share of profit or loss, interest on capital, drawings, interest on drawings etc. are recorded in the partners' capital accounts.

Choose the correct option from the following:

Calculate ‘Cash Flows from Financing Activities’ from the following information:

Additional Information:

(i) Interest paid on bank loan amounted to ₹ 60,000.

(ii) Dividend paid ₹ 1,10,000.

Calculate ‘Cash Flows from Investing Activities’ from the following information:

Additional Information:

(a) A machine costing ₹ 85,000 (depreciation provided thereon ₹ 15,000) was sold for ₹ 62,000. Depreciation charged during the year amounted to ₹ 48,000.

Statement II: ‘Cash withdrawn from bank’ will result in inflow of cash.

(b) Prepare oss on Issue of Debentures Account for the year ended 31st March, 2023.}

- Plant and Machinery was taken over by Abhay at an agreed valuation of ₹ 75,000.

- Furniture realised ₹ 40,000.

- Motor Car was taken over by Bikram for ₹ 1,30,000.

- Debtors realised 10% less than their book value.

- 10% of the stock was taken over by Chris for ₹ 4,500. The remaining stock was sold for ₹ 30,000.

- Realisation expenses amounted to ₹ 5,000.

Record necessary journal entries in the books of Gundola Ltd. for the above transactions.

Pass necessary journal entries for the above transactions in the books of Sumi Ltd.

Options:

Options:

(a) Loose Tools

(b) Provision for Tax

(c) Copyrights

Statement II: ‘Cash withdrawn from bank’ will result in inflow of cash.

In the context of the above two statements, choose the correct option:

\hline Capital: & & Fixed Assets & 1,20,000

Inder & 90,000 & Stock & 60,000

Jonny & 75,000 & Debtors & 1,00,000

Kapil & 60,000 & Cash & 35,000

\hline General Reserve & 80,000 & &

Creditors & 10,000 & &

\hline Total & 3,15,000 & Total & 3,15,000

\hline \end{tabular} \end{center} Adjustments on Kapil’s Retirement: Bad debts amounting to ₹ 5,000 were written off. Fixed Assets were revalued at ₹ 96,000. Stock was undervalued by ₹ 29,000. Creditors were paid off. Goodwill of the firm was valued at ₹ 80,000, and Kapil’s share of goodwill was adjusted in the accounts of Inder and Jonny. New profit-sharing ratio between Inder and Jonny = .

\text{On application : ₹ 4 \text{ per share}

\text{On allotment} : ₹ 4 \text{ per share}

\text{On first and final call} : \text{Balance}.}

The issue was fully subscribed. All the amounts were duly received except the first and final call money on 4,000 equity shares. Show the Share Capital in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013. Also prepare ‘Notes to Accounts’ for the same.

Choose the correct option from the following:

(i) respective unpaid calls account i.e., calls in arrears and

(ii) share forfeiture account with the amount already received on shares.

Reason (R): When the shares are forfeited, all entries relating to the shares forfeited, except those relating to securities premium, already recorded in accounting records must be reversed.

On application and allotment — ₹ 7 per share (including premium)

On first and final call — Balance

The issue was fully subscribed. All the money was duly received except the first and final call on 1,000 equity shares. These shares were forfeited. On forfeiture of these shares, Calls in Arrears Account will be:

- Interest paid on bank loan amounted to ₹ 60,000.

- Dividend paid ₹ 1,10,000.

- A machine costing ₹ 85,000 (depreciation provided thereon ₹ 15,000) was sold for ₹ 62,000.

- Depreciation charged during the year amounted to ₹ 48,000.

(b) Loose Tools

(c) Income Received in Advance

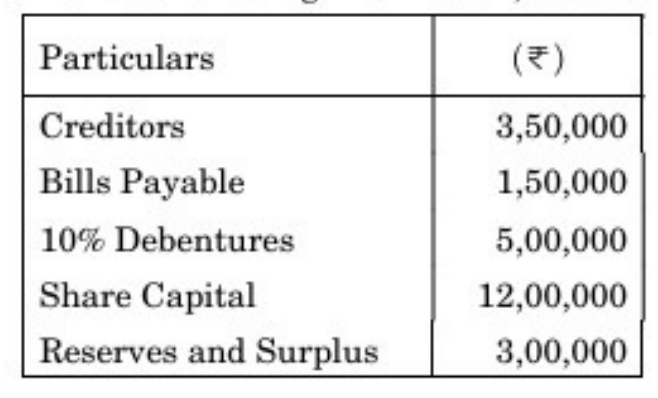

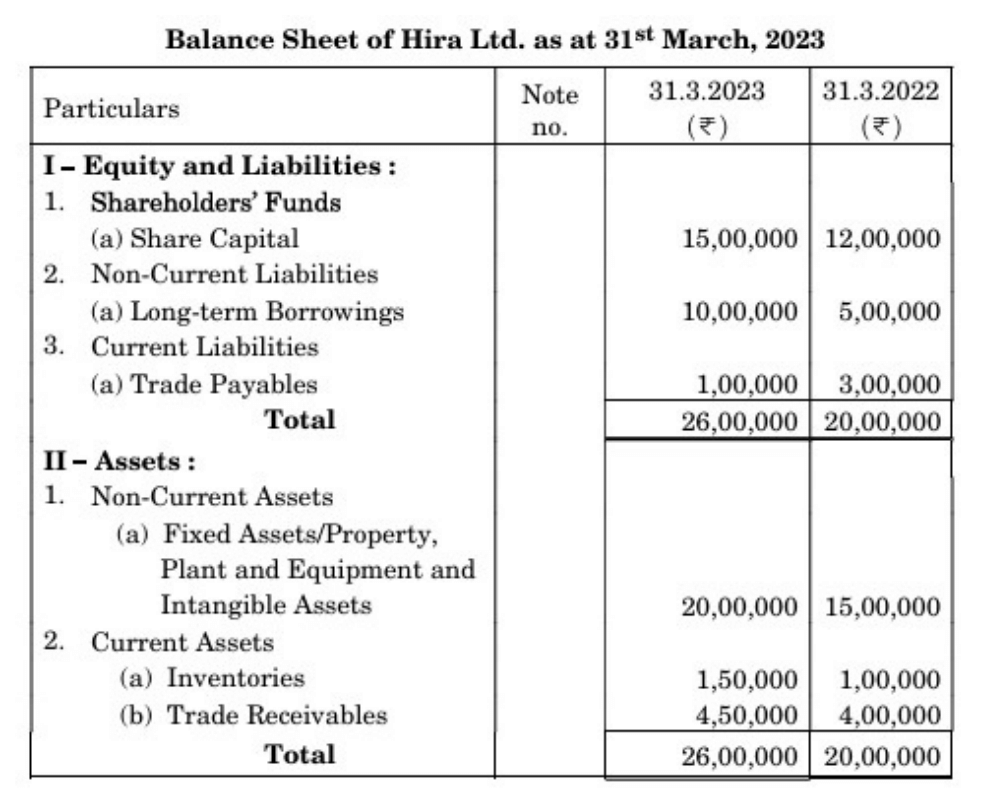

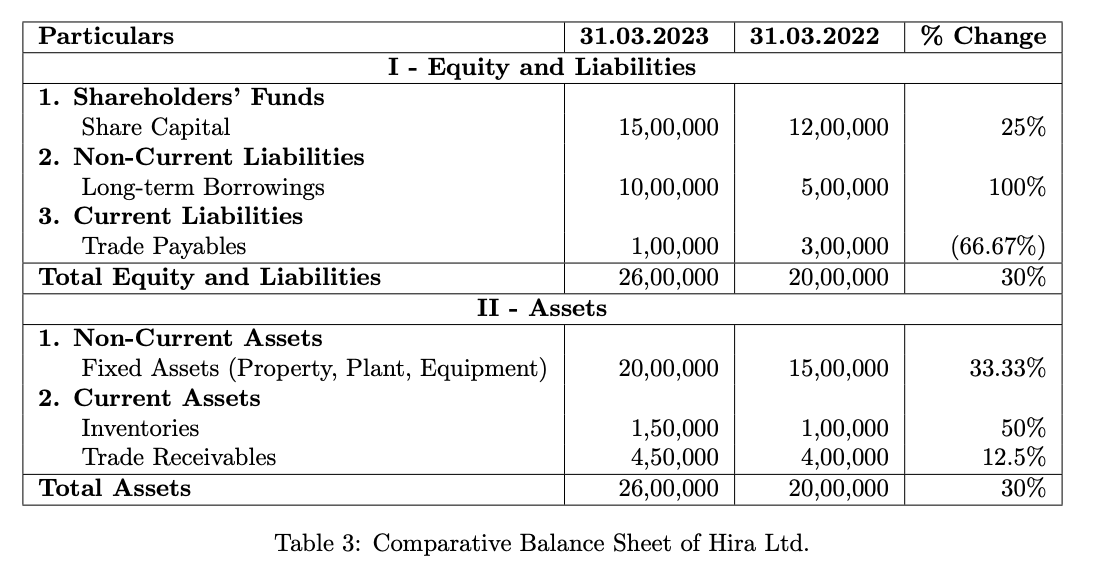

From the following Balance Sheet of Hira Ltd. as at 31st March, 2023, prepare Comparative Balance Sheet:

About Miscellaneous - CBSE-CLASS-XII

Miscellaneous is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Miscellaneous PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Miscellaneous carry the most weight. Then, tackle the questions iteratively to solidify your understanding.