Partnership

67 previous year questions.

High-Yield Trend

Chapter Questions 67 MCQs

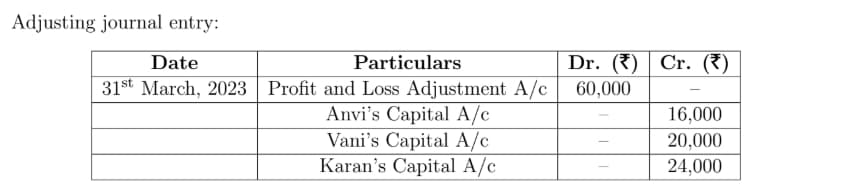

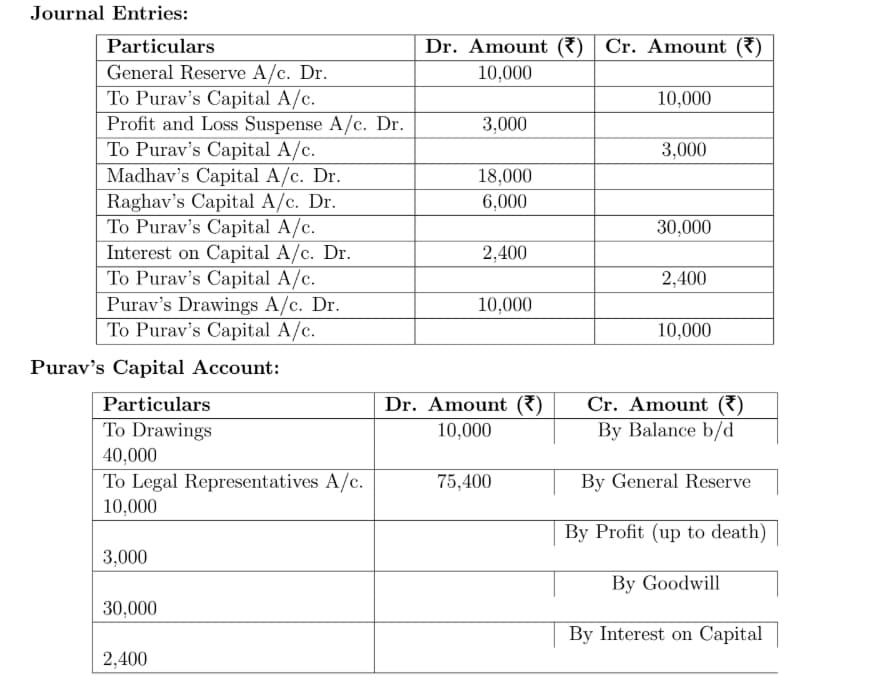

Purav died on 30th September, 2023. According to Partnership deed, his legal representatives are entitled to the following:

(i) Balance in his Capital Account.

(ii) Share of profit up to the date of death to be calculated on the basis of last year’s profit.

(iii) Share of goodwill calculated on the basis of three years purchase of average profits of last four years.

(iv) Interest on capital @12% p.a.

Purav’s share of profit was |3,000, and the average profit of the last four years was |50,000. Purav’s drawings up to the date of death were |10,000. Prepare Purav’s Capital Account to be rendered to his legal representatives.

Aakash and Baadal entered into partnership on 1st October 2023 with capitals of Rs 80,00,000 and Rs 60,00,000 respectively. They decided to share profits and losses equally. Partners were entitled to interest on capital @ 10 per annum as per the provisions of the partnership deed. Baadal is given a guarantee that his share of profit, after charging interest on capital, will not be less than Rs 7,00,000 per annum. Any deficiency arising on that account shall be met by Aakash. The profit of the firm for the year ended 31st March 2024 amounted to Rs 13,00,000.

Prepare Profit and Loss Appropriation Account for the year ended 31st March 2024.

C was to be given a commission of ₹ 5,000 p.a.

Interest on capital was to be allowed @ 10% p.a.

A was to be given a salary of ₹ 1,000 p.m.

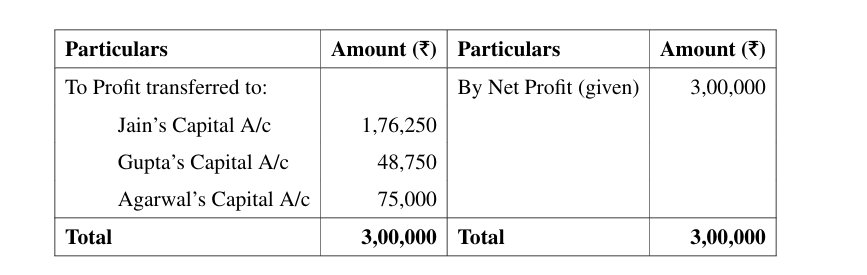

The net profit of the firm for the year ended 31st March, 2024 before providing for any of the above was ₹ 75,000. The net profit to be distributed among partners will be :

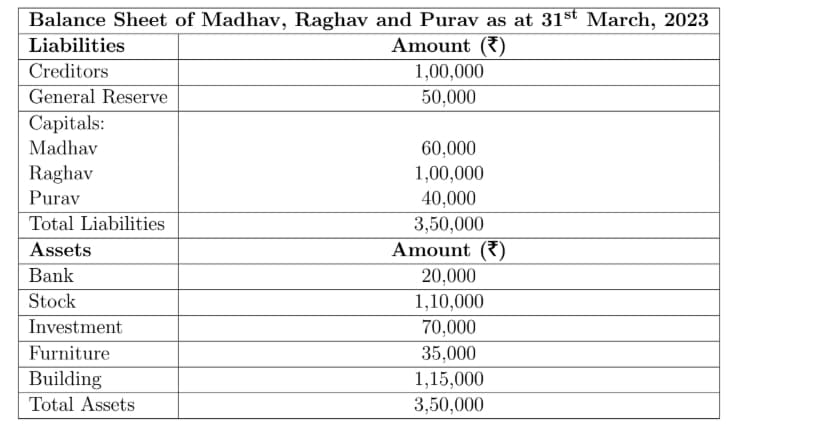

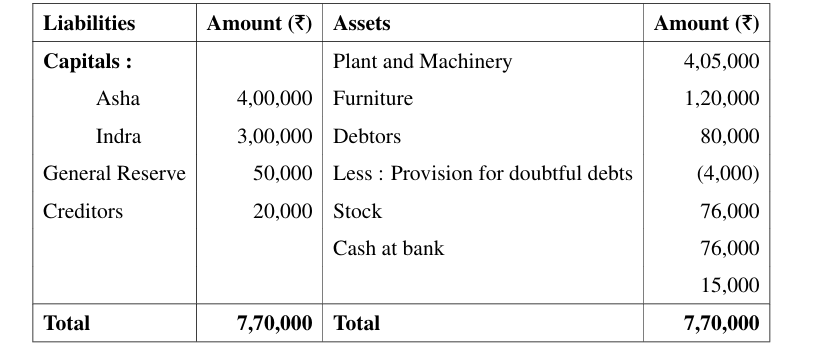

Balance Sheet of Raja, Bharat and Vedika as on 31st March, 2024

| Liabilities Amount (₹) | Amount (₹) | Assets |

|---|---|---|

| Creditors | 80,000 | Bank |

| General Reserve | 50,000 | Stock |

| Capitals: Raja Bharat Vedika | 1,10,000 1,00,000 90,000 | Debtors Furniture Machinery |

| Total | 4,30,000 | Total |

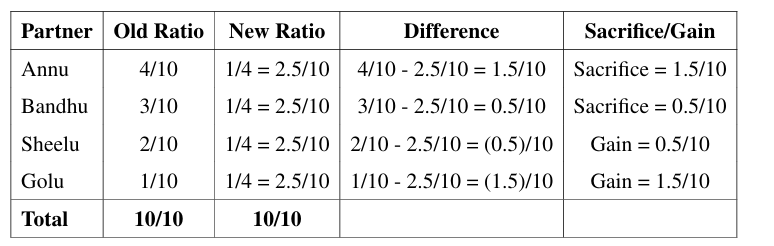

Naval, Nyaya and Nritya were partners sharing profits in the ratio of 3:5:2. On 31st March, 2024, Nyaya retired. Revaluation of assets and goodwill adjustments were made. Prepare Revaluation Account and Partners’ Capital Accounts.

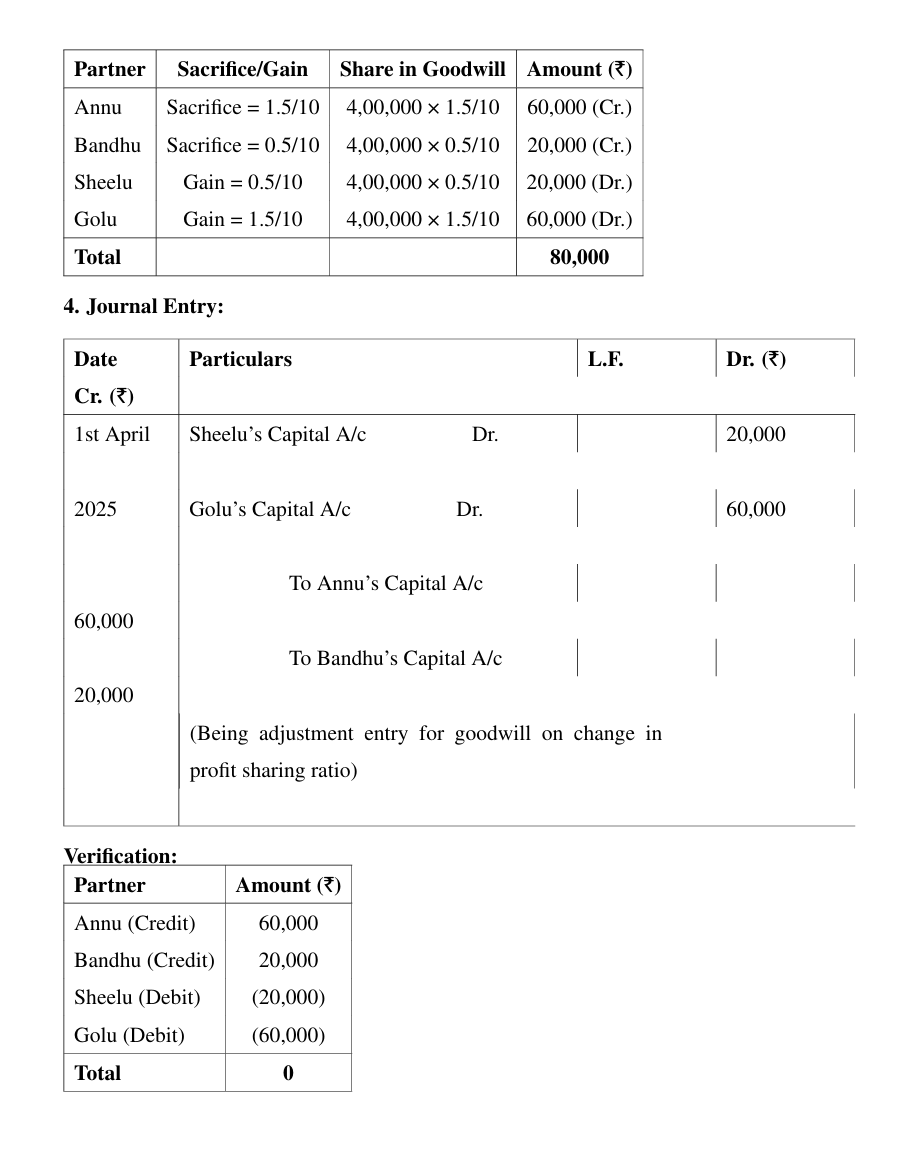

Pass necessary journal entries for the above transactions on the reconstitution of the firm. Show your workings clearly.

Reason (R): By virtue of the Companies Act 2013, the Central Government is empowered to prescribe maximum number of partners in a firm. The Central Government has prescribed the maximum number of partners in a firm to be 50.

Choose the correct option from the following:

Wayne, Shaan and Bryan were partners in a firm. Shaan had advanced a loan of Rs 1,00,000 to the firm. On 31st March, 2024 the firm was dissolved. After transferring various assets (other than cash & bank) and outside liabilities to Realisation Account, Shaan took over furniture of book value of Rs 90,000 in part settlement of his loan amount. For the payment of balance amount of Shaan's loan Bank Account will be credited with:

Uma and Umesh were partners in a firm sharing profits and losses in the ratio of 2:3. On 31st March, 2024, their Balance Sheet was given. Daya was admitted with 2:3:5 profit sharing ratio, bringing in capital and goodwill. Various revaluations and adjustments were also made. Journalise the transactions related to Daya’s admission.

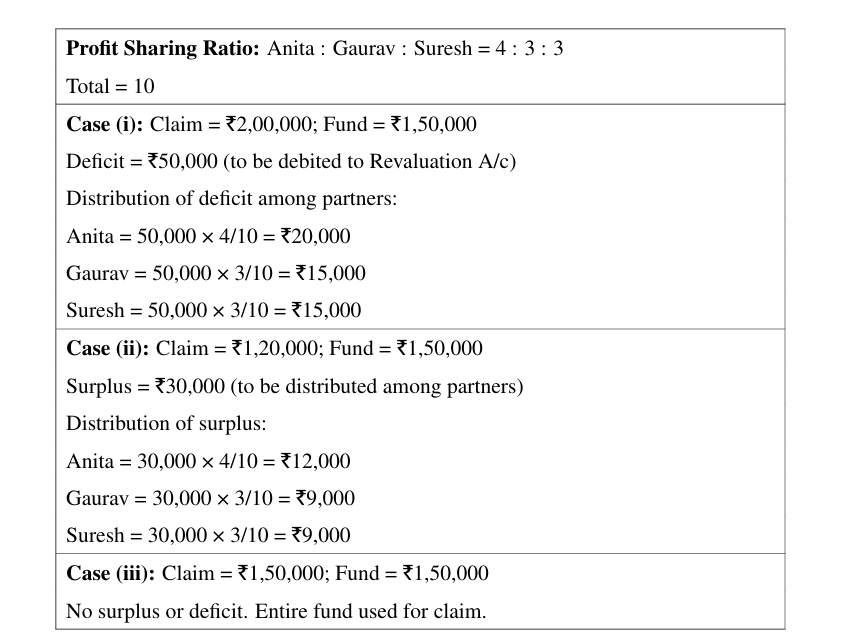

Rani, Manav and Pushpa were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. On 1st April, 2024, Rani decided to retire from the firm. On that day, the balance in her capital account after making necessary adjustments on account of reserves, revaluation of assets and reassessment of liabilities was 3,08,000. Manav and Pushpa agreed to pay her 3,80,000 in full settlement of her claim.

Calculate Rani’s share of goodwill and pass the necessary journal entry for the same.

Jim and Joy were partners in a firm sharing profits and losses equally. On 1st April, 2024, they admitted John as a new partner for share in the profits of the firm. On the date of John’s admission, the Balance Sheet of Jim and Joy showed a debit balance of 45,000 in the Profit and Loss Account.

From the following, what will be the accounting treatment for this balance on John’s admission?

Vimal, Bose and Ghosh were partners in a firm sharing profits and losses equally. On 1st April, 2024, Bose retired from the firm and the new profit sharing ratio between Vimal and Ghosh was decided as 4 : 3. On Bose’s retirement, the goodwill of the firm was valued at 2,10,000. It was decided to treat goodwill without opening goodwill account. By what amount will the partners’ capital accounts be debited or credited for the treatment of goodwill on Bose’s retirement?

Hari, Chander, Prakash and Govind were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 1 : 1. On 1st April, 2024, Hari retired and his share was acquired equally by Chander, Prakash and Govind. The new profit sharing ratio of Chander, Prakash and Govind will be:

Saloni and Mohini were partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2024, Saloni’s capital was 1,50,000. During the year, she withdrew 10,000 and introduced additional capital of 32,000. For the year ended 31st March, 2024, the firm earned a profit of 50,000. Saloni’s capital as on 1st April, 2023, was:

Revaluation A/c Dr. 30,000

To Provision for Bad Debts 30,000

Revaluation A/c Dr. 6,000

To Provision for Bad Debts 6,000

Govindan’s A/c Dr. 2,000

To Provision for Bad Debts 2,000

Nandan’s A/c Dr. 2,000

Abhinandan’s A/c Dr. 2,000

Govindan’s A/c Dr. 2,000

To Provision for Bad Debts 6,000

Pooja and Kumari were partners in a firm sharing profits and losses in the ratio of 2 : 1. On 1st April, 2023, Noori was admitted for a new partner share in the profits of the firm. Noori was guaranteed a minimum profit of 1,20,000. Any deficiency on this account was to be borne by Pooja and Kumari in their profit sharing ratio. During the year ended 31st March, 2024, the firm earned a net profit of 3,60,000. The amount of deficiency borne by Pooja will be:

Pass necessary journal entries for the above transactions in the books of the firm on Rishab’s admission.

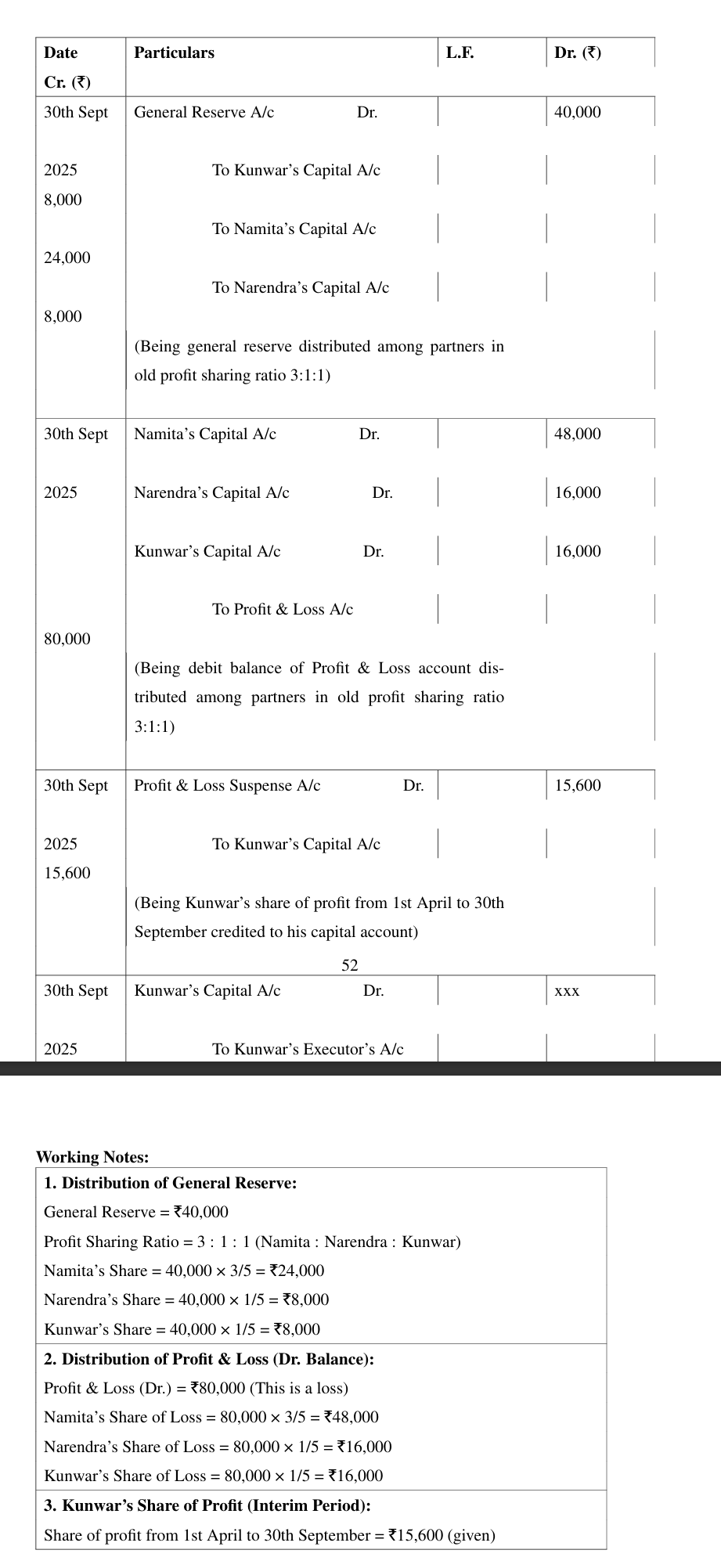

Hans, Sohan and Kishore were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. The firm closes its books on 31st March every year. On 1st August, 2024, Kishore died. The partnership deed provided that on the death of a partner, his executors will be entitled for:

(i) Balance in his capital account less drawings.

(ii) Interest on capital @ 12% p.a.

(iii) His share of goodwill.

(iv) His share in the profits of the firm till the date of his death calculated on the basis of average profit of the previous four years.

The following information was obtained from the books of the firm on the date of Kishore’s death:

(a) Capital on 1st April, 2024 = 4,00,000, Drawings = 90,000

(b) Goodwill of the firm = 60,000

(c) Profits for last 4 years: 2,00,000, 2,20,000, 1,20,000, 1,80,000

Jain and Gupta were partners in a firm sharing profits and losses in the ratio of 7 : 3. On 31st March, 2024, the firm was dissolved. After transferring various assets (other than cash 6,400) and the third-party liabilities to Realisation Account, the following transactions took place:

- [(i)] Debtors 80,000 were taken over by a debt collection agency at 10% discount.

- [(ii)] Creditors amounting to 40,000 were taken over by Jain.

- [(iii)] Realisation expenses amounted to 5,100, which were paid by Gupta.

Pass necessary journal entries for the above transactions in the books of Jain and Gupta.

Assertion (A): Private assets of a partner can also be used for paying off the firm’s debts.

Reason (R): Liability of a partner for acts of the firm is limited.

Choose the correct alternative from the following:

\hline Creditors & 4,20,000 & Cash at Bank & 3,10,000

Mrs. Guru’s Loan & 5,00,000 & Stock & 6,00,000

Samta’s Loan & 4,40,000 & Debtors & 3,90,000

& & Less: Provision for doubtful debts & (10,000)

& & & 3,80,000

Capitals: & & Land and Building & 4,14,000

Guru & 3,00,000 & Plant and Machinery & 9,00,000

Samta & 5,00,000 & &

Prakash & 4,44,000 & &

\cline{2-2} Total & 26,04,000 & Total & 26,04,000

\hline \end{tabular} On the above date the firm was dissolved and the following transactions took place :

(i) Debtors were taken over by creditors in full settlement of their account.

(ii) 50% of stock was taken over by Samta at 10% less than book value. Remaining stock sold at 20% profit.

(iii) Land and Building taken over by Prakash for ₹ 20,00,000.

Plant and Machinery sold as scrap for ₹ 1,00,000.

(iv) Guru agreed to pay off Mrs. Guru’s loan.

(v) Realisation expenses amounted to ₹ 56,000.

Prepare the Realisation Account.

Prepare Rohit’s Loan Account till it is fully paid.

\textbf{Correct Answer:} (C)

[(i)] During the year ended 31st March, 2024, the firm earned a profit of ₹ 3,00,000.

[(ii)] During the year ended 31st March, 2024, the firm earned a profit of ₹ 1,20,000.

Assertion (A): At the time of admission of a new partner in a partnership firm, the newly admitted partner brings an agreed amount of capital either in cash or in kind.

Reason (R): On admission, the new partner gets the right to acquire share in the assets and profits of the partnership firm.

Choose the correct option from the following:

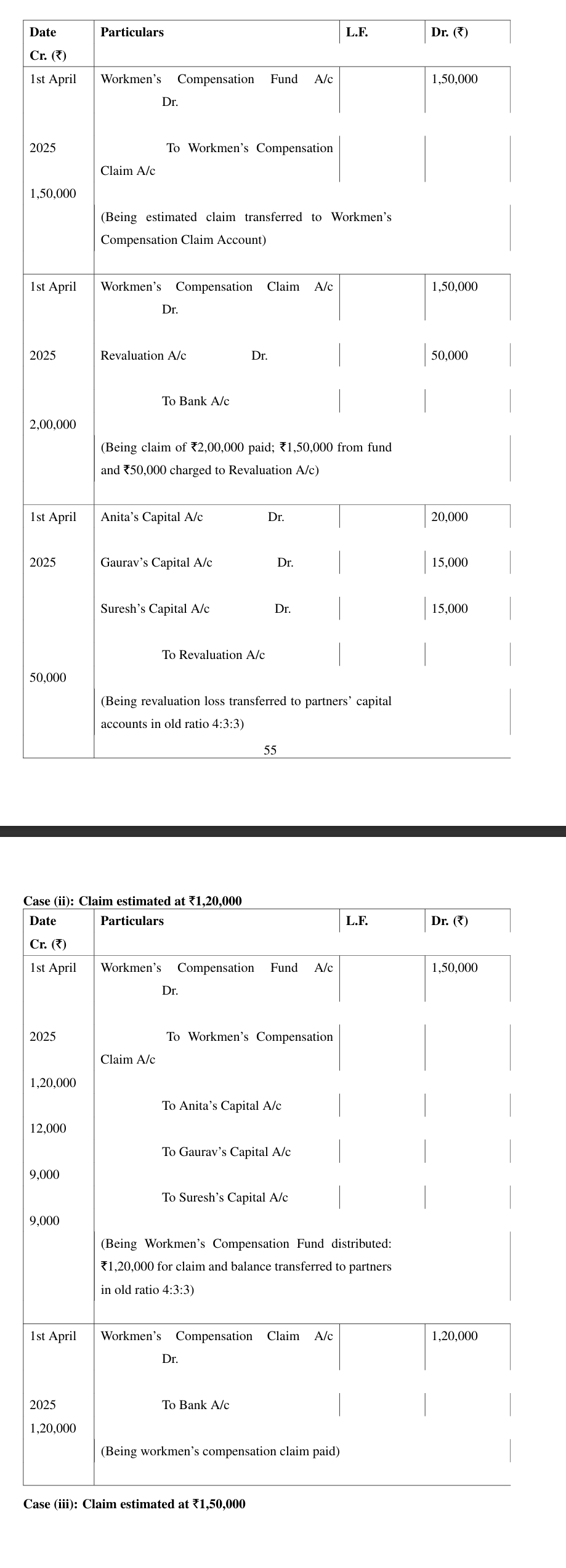

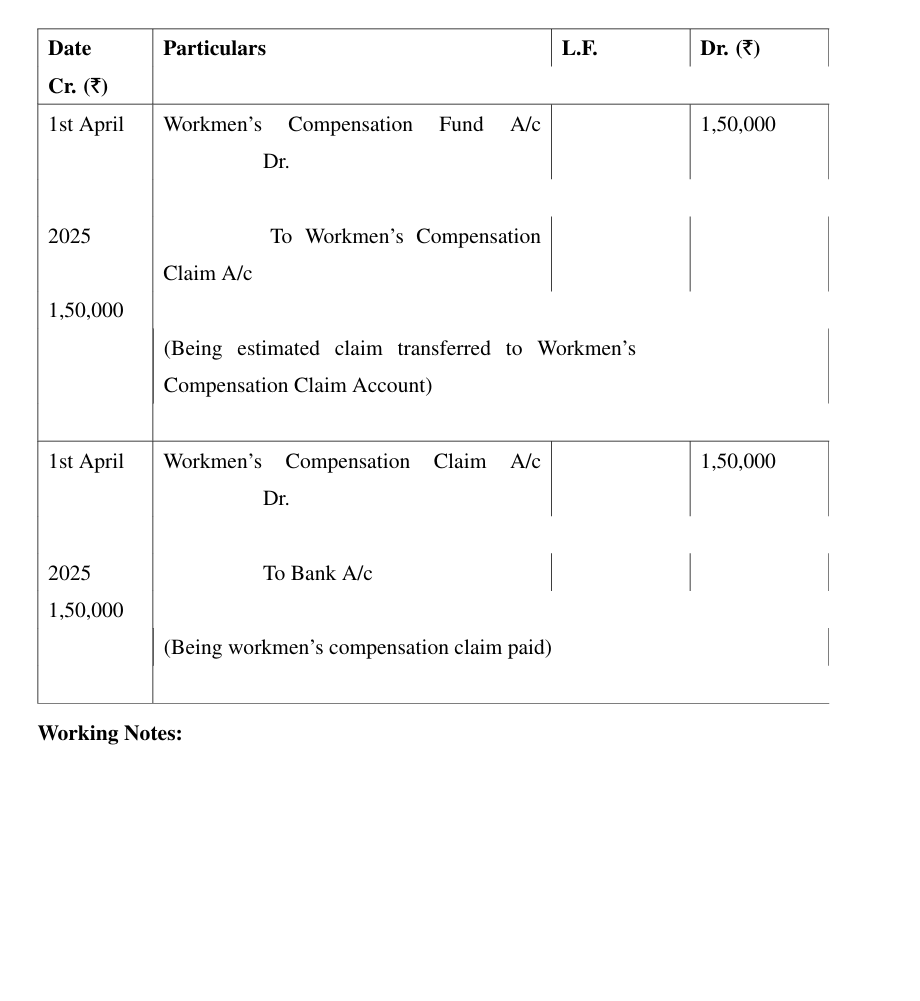

- [(i)] Claim on account of Workmen’s Compensation was estimated at ₹ 1,20,000.

- [(ii)] Claim on account of Workmen’s Compensation was estimated at ₹ 80,000.

- [(iii)] Claim on account of Workmen’s Compensation was estimated at ₹ 1,00,000.

Preference Share Capital ₹1,00,000

Reserves and Surplus ₹1,00,000

Plant and Machinery ₹3,50,000

Non-current Investments ₹1,00,000

Current Assets ₹2,00,000

Long-term Borrowings ₹1,50,000

\hline Rent received in advance & 20,000 & 10,000

Accrued interest & 30,000 & 40,000

Prepaid insurance & 15,000 & 20,000

Outstanding salary & 25,000 & 40,000

Trade receivables & 1,24,000 & 1,25,000

Trade payables & 1,30,000 & 1,50,000

Inventory & 50,000 & 80,000

Other current assets & 1,00,000 & 1,20,000

\hline \end{tabular} \end{center}

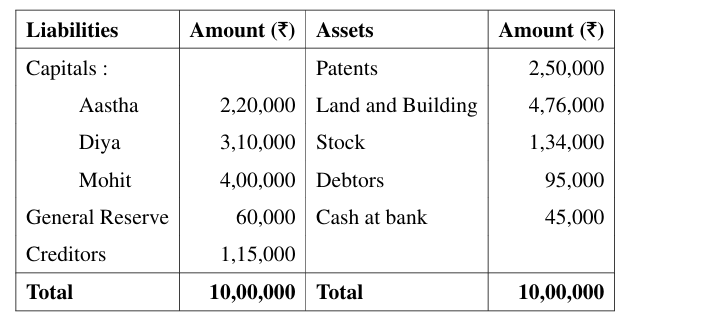

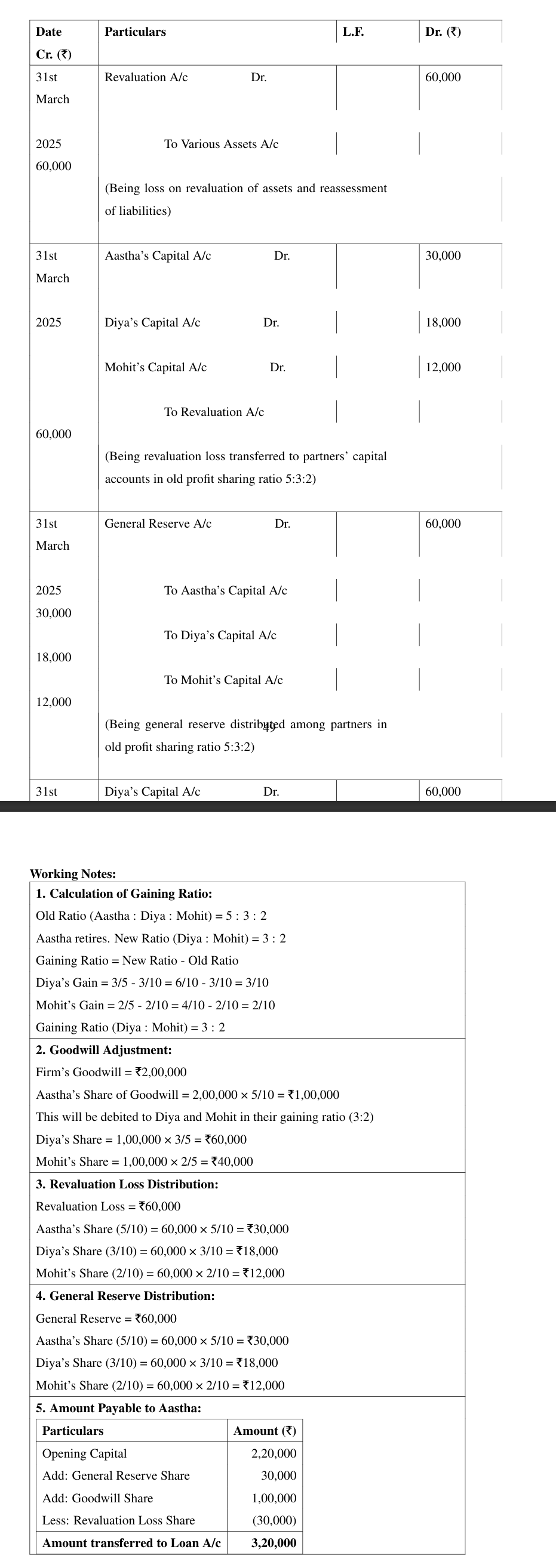

- [(i)] Goodwill of the firm was valued at ₹ 2,00,000 and the same was to be treated without opening goodwill account.

- [(ii)] Revaluation of assets and reassessment of liabilities resulted in a loss of ₹ 60,000.

- [(iii)] Amount payable to Aastha was transferred to her loan account.

About Partnership - CBSE-CLASS-XII

Partnership is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Partnership PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Partnership carry the most weight. Then, tackle the questions iteratively to solidify your understanding.