Partnership Accounts

51 previous year questions.

High-Yield Trend

Chapter Questions 51 MCQs

Assertion (A): Securities Premium cannot be utilized for writing off loss on sale of a fixed asset.

Reason (R): Securities Premium can be applied only for the purposes mentioned in the Companies Act, 2013.

Choose the correct option from the following:

Manav’s Capital A/c Dr. ₹30,000

Mayank’s Capital A/c Dr. ₹18,000

Manish’s Capital A/c Dr. ₹12,000

To Profit and Loss A/c ₹60,000

Manav’s Capital A/c Dr. ₹24,000

Mayank’s Capital A/c Dr. ₹24,000

Manish’s Capital A/c Dr. ₹12,000

To Profit and Loss A/c ₹60,000

Mayank’s Capital A/c Dr. ₹6,000

To Manav’s Capital A/c ₹6,000

Manav’s Capital A/c Dr. ₹6,000

To Mayank’s Capital A/c ₹6,000

The following journal entry appears in the books of Latvion Ltd.:

| Date | Particulars | Dr. Amount (₹) | Cr. Amount (₹) |

| Bank A/c | 4,75,000 | ||

| Loss on issue of debentures A/c | 75,000 | ||

| To 12% Debentures A/c | 5,00,000 | ||

| To Premium on Redemption of Debentures A/c | 50,000 |

The discount on issue of debentures is:

The amount of interest allowed on Tara’s capital for the year ended 31st March, 2024 was :

(i) Rajesh took over stock of Rs 4,00,000 at a discount of 20\%.

(ii) Somesh agreed to take over the firm's furniture, not recorded in the books of the firm at Rs 80,000.

(iii) Land and Building of the book value of Rs 60,00,000 was sold for Rs 90,00,000 through a broker who charged 10\% commission.

(iv) Ashish, an old customer, whose account for Rs 70,000 was written off as bad in the previous year, paid 60\% of the amount.

(v) Sundry Creditors of Rs 3,00,000 were settled at a discount of 10\%.

(vi) Realisation expenses amounting to Rs 21,000 were paid by Yogesh.

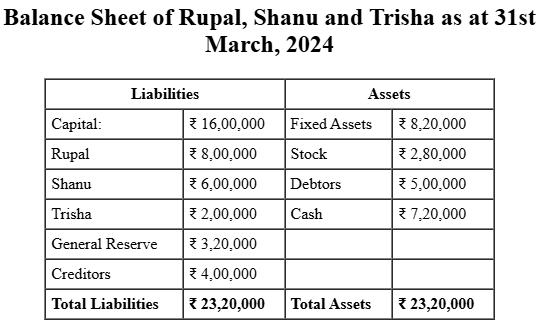

Rupal, Shanu and Trisha were partners in a firm sharing profits and losses in the ratio of 4:3:1. Their Balance Sheet as at 31st March, 2024 was as follows:

(i) Trisha's share of profit was entirely taken by Shanu.

(ii) Fixed assets were found to be undervalued by Rs 2,40,000.

(iii) Stock was revalued at Rs 2,00,000.

(iv) Goodwill of the firm was valued at Rs 8,00,000 on Trisha's retirement.

(v) The total capital of the new firm was fixed at Rs 16,00,000 which was adjusted according to the new profit sharing ratio of the partners. For this necessary cash was paid off or brought in by the partners as the case may be.

Prepare Revaluation Account and Partners' Capital Accounts.

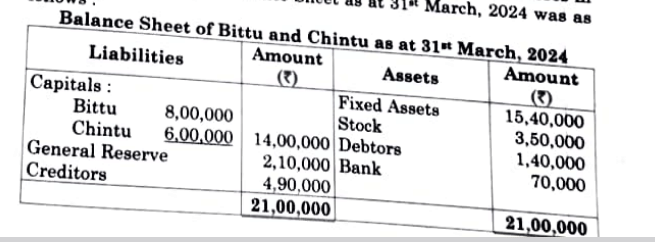

Bittu and Chintu were partners in a firm sharing profit and losses in the ratio of 4 : 3. Their Balance Sheet as at 31st March, 2024 was as follows:

On 1st April, 2024, Diya was admitted in the firm for th share in the profits on the following terms:

- (i) New profit sharing ratio between Bittu, Chintu and Diya was 3 : 3 : 1 .

- (ii) Fixed Assets were found to be overvalued by ₹ 1,40,000.

- (iii) Creditors were paid ₹ 4,20,000 in full settlement.

- (iv) Diya brought proportionate capital and ₹ 5,60,000 as her share of goodwill premium by cheque.

Prepare Revaluation Account and Partners' Capital Accounts.

Reason (R): There exists a relationship of mutual agency between all the partners.

Choose the correct option from the following:

Balance sheet of Simar, Tanvi and Umara as at 31st March, 2024

% [Balance Sheet Table - Simplified representation below] % Liabilities: Capitals (S:13L, T:12L, U:14L) = 39L; General Reserve = 7L; Trade Payables = 6L; Total = 52L % Assets: Fixed Assets = 25L; Stock = 10L; Debtors = 8L; Cash = 7L; P A/c (2023-24) = 2L; Total = 52L Liabilities: Capitals (S:13L, T:12L, U:14L) 39L, General Reserve 7L, Trade Payables 6L. Total 52L.

Assets: Fixed Assets 25L, Stock 10L, Debtors 8L, Cash 7L, Profit and Loss Account (2023-24) 2L. Total 52L.

\textbf{Umara died on 30th June, 2024. The partnership deed provided for the following on the death of a partner:

Pass necessary journal entries for the above transactions on the reconstitution of the firm. Show your working clearly.

Bittu and Chintu were partners in a firm sharing profits and losses in the ratio of 4 : 3. Their Balance Sheet as at 31st March, 2024 was as follows:

Balance Sheet of Bittu and Chintu as at 31st March, 2024

| Liabilities | Amount (₹) | Assets | Amount (₹) |

| Capitals: | Fixed Assets | 15,40,000 | |

| Bittu | 8,00,000 | Stock | 3,50,000 |

| Chintu | 6,00,000 | Debtors | 1,40,000 |

| General Reserve | 2,10,000 | Bank | 70,000 |

| Creditors | 4,90,000 | ||

| Total | 21,00,000 | Total | 21,00,000 |

On 1st April, 2024, Diya was admitted in the firm for 1⁄7 share in the profits on the following terms:

- New profit sharing ratio between Bittu, Chintu, and Diya will be 3 : 3 : 1.

- Fixed Assets were found to be overvalued by ₹ 1,40,000.

- Creditors were paid ₹ 4,20,000 in full settlement.

- Diya brought proportionate capital and ₹ 5,60,000 as her share of goodwill premium by cheque.

Prepare Revaluation Account and Partners’ Capital Accounts.

(ii) Pass journal entries for goodwill treatment in the books of the firm

[(i)] During the year ended 31st March, 2024, the firm earned a profit of ₹ 2,00,000.

[(ii)] During the year ended 31st March, 2024, the firm earned a profit of ₹ 66,000.

On Application – ₹20

On Allotment – ₹50

On First and Final Call – Balance

Applications for 2,00,000 shares were received. An applicant who had applied for 5,000 shares paid the entire share money with the application.

The total application money received by the company was:

The partnership deed provided for the following on the death of a partner: (i) Balance in her capital account.

(ii) Interest on capital @ 12% p.a.

(iii) Her share in the profits of the firm till the date of her death calculated on the basis of previous year’s profits. The profit of the firm for the year ended 31st March, 2024 was \rupee~2,80,000.

(iv) Her share in the goodwill of the firm. The goodwill of the firm on Kalyani’s death was valued at \rupee~4,00,000.

Prepare Kalyani’s Capital Account to be presented to her executors.

Reason (R): By virtue of the Companies Act 2013, the Central Government is empowered to prescribe maximum number of partners in a firm. The Central Government has prescribed the maximum number of partners in a firm to be 50.

Choose the correct option from the following:

2021–22 ₹ 60,000

2022–23 ₹ 90,000

2023–24 ₹ 1,20,000

Calculate goodwill of the firm on the following basis:

[(i)] Four years purchase of the average profits for the last three years

[(ii)] Capitalisation of super-profits

Sudha and Sudhir were partners in a firm sharing profits and losses in the ratio of 4 : 1. On 1st April, 2023, their fixed capitals were ₹12,00,000 and ₹4,00,000 respectively. On 1st July, 2023, Sudha invested ₹2,00,000 as additional capital. On 1st August, 2023, Sudhir withdrew ₹50,000 from his capital.

The partnership deed provided for the following:

(i) Interest on capital @ 6% p.a.

(ii) Interest on drawings @ 8% p.a.

During the year, Sudha withdrew ₹60,000 and Sudhir withdrew ₹40,000 for personal use. After providing interest on capital and charging interest on drawings, the net profit of the firm for the year ended 31st March, 2024 was ₹3,50,000.

Prepare Current Accounts of Sudha and Sudhir.

Pass necessary journal entries for treatment of provision for bad and doubtful debts on the date of Rishi’s admission in each of the following cases:

(i) Bad debts amounted to ₹ 60,000.

(ii) Bad debts amounted to ₹ 90,000.

(iii) Bad debts amounted to ₹ 1,00,000.

About Partnership Accounts - CBSE-CLASS-XII

Partnership Accounts is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Partnership Accounts PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Partnership Accounts carry the most weight. Then, tackle the questions iteratively to solidify your understanding.