Profit And Loss Account

12 previous year questions.

High-Yield Trend

Chapter Questions 12 MCQs

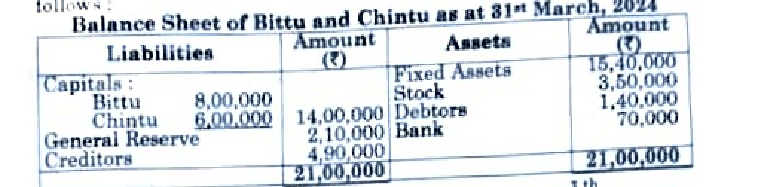

Bittu and Chintu were partners in a firm sharing profit and losses in the ratio of 4:3. Their Balance Sheet as at 31st March, 2024 was as

On April, 2024, Diya was admitted in the firm for share in the profits on the following terms:

- New profit sharing ratio between Bittoo, Chintoo and Diya will be .

- Fixed Assets were found to be overvalued by ₹ 1,40,000.

- Creditors were paid ₹ 4,20,000 in full settlement.

- Diya brought proportionate capital and ₹ 5,60,000 as her share of goodwill premium by cheque.

Prepare Revaluation Account and Partners' Capital Accounts.

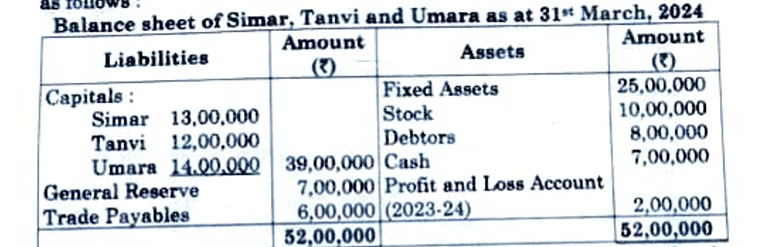

Simar, Tanvi and Umara were partners in a firm sharing profits and losses in the ratio of 5:6:9. On 31st March, 2024 their Balance Sheet was as follows:

Umara died on 30th June, 2024. The partnership deed provided for the following on the death of a partner:

7:3

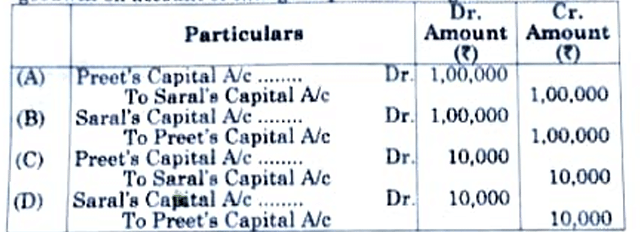

Preet and Saral were partners sharing profits and losses in the ratio of 3:2. On 31st March, 2024 they decided to change their profit sharing ratio to 1:1. On the date of reconstitution goodwill of the firm was valued at Rs 1,00,000. The journal entry for treatment of goodwill on account of change in profit-sharing ratio will be:

Simar, Tanvi, and Umara were partners in a firm sharing profits and losses in the ratio of 5 : 6 : 9. On 31st March, 2024, their Balance Sheet was as follows:

Balance Sheet of Simar, Tanvi, and Umara as at 31st March, 2024

| Liabilities | Amount (₹) | Assets | Amount (₹) |

| Capitals: | Fixed Assets | 25,00,000 | |

| Simar | 13,00,000 | Stock | 10,00,000 |

| Tanvi | 12,00,000 | Debtors | 8,00,000 |

| Umara | 14,00,000 | Cash | 7,00,000 |

| General Reserve | 7,00,000 | Profit and Loss A/c | 2,00,000 |

| Trade Payables | 6,00,000 | ||

| Total | 52,00,000 | Total | 52,00,000 |

Umara died on 30th June, 2024. The partnership deed provided for the following on the death of a partner:

- Goodwill of the firm be valued at 3 years purchase of average profits for the last 5 years. The profits/losses for the previous four years were:

- 2022-23: ₹ 3,10,000 (loss)

- 2021-22: ₹ 3,00,000 (profit)

- 2020-21: ₹ 4,00,000 (profit)

- 2019-20: ₹ 2,50,000 (profit)

- Umara’s share of profit or loss till the date of her death was to be calculated on the basis of profit or loss for the year ended 31st March 2024.

- Calculate Goodwill of the firm.

- Pass the necessary journal entry for the treatment of goodwill on Umara’s death.

- Calculate Umara’s share in the profit or loss of the firm till the date of her death.

- Pass the necessary journal entry to record Umara’s share of profit or loss till the date of her death.

From the following information, prepare a Comparative Statement of Profit and Loss for the year ended March, 2024 :

| Particulars | 2023-24 (₹) | 2022-23 (₹) |

| Revenue from operations | 8,00,000 | 4,00,000 |

| Cost of revenue from operations | 4,00,000 | 2,00,000 |

| Employee benefit expenses | 1,60,000 | 80,000 |

| Tax Rate | 50% |

(a) From the following information, calculate Opening Trade Receivables and Closing Trade Receivables :

- Trade Receivables Turnover Ratio = 4 times

- Closing Trade Receivables were ₹ 20,000 more than that in the beginning.

- Cost of Revenue from operations = ₹ 6,40,000.

- Cash Revenue from operations = of Credit Revenue from Operations

- Gross Profit Ratio = 20%

About Profit And Loss Account - CBSE-CLASS-XII

Profit And Loss Account is a vital chapter for CBSE-CLASS-XII aspirants. Mastering the concepts covered in this chapter is essential for securing a top rank.

By rigorously practicing the previous year questions associated with this chapter, you can identify high-yield topics, understand the examiner's perspective, and boost your confidence during the actual exam.

Frequently Asked Questions

Why focus on Profit And Loss Account PYQs?

Analyzing PYQs for this specific chapter reveals the most frequently tested concepts and the typical complexity of questions, allowing you to tailor your study plan efficiently.

How to best use this analysis?

Review the topic breakdown to see which sub-topics within Profit And Loss Account carry the most weight. Then, tackle the questions iteratively to solidify your understanding.